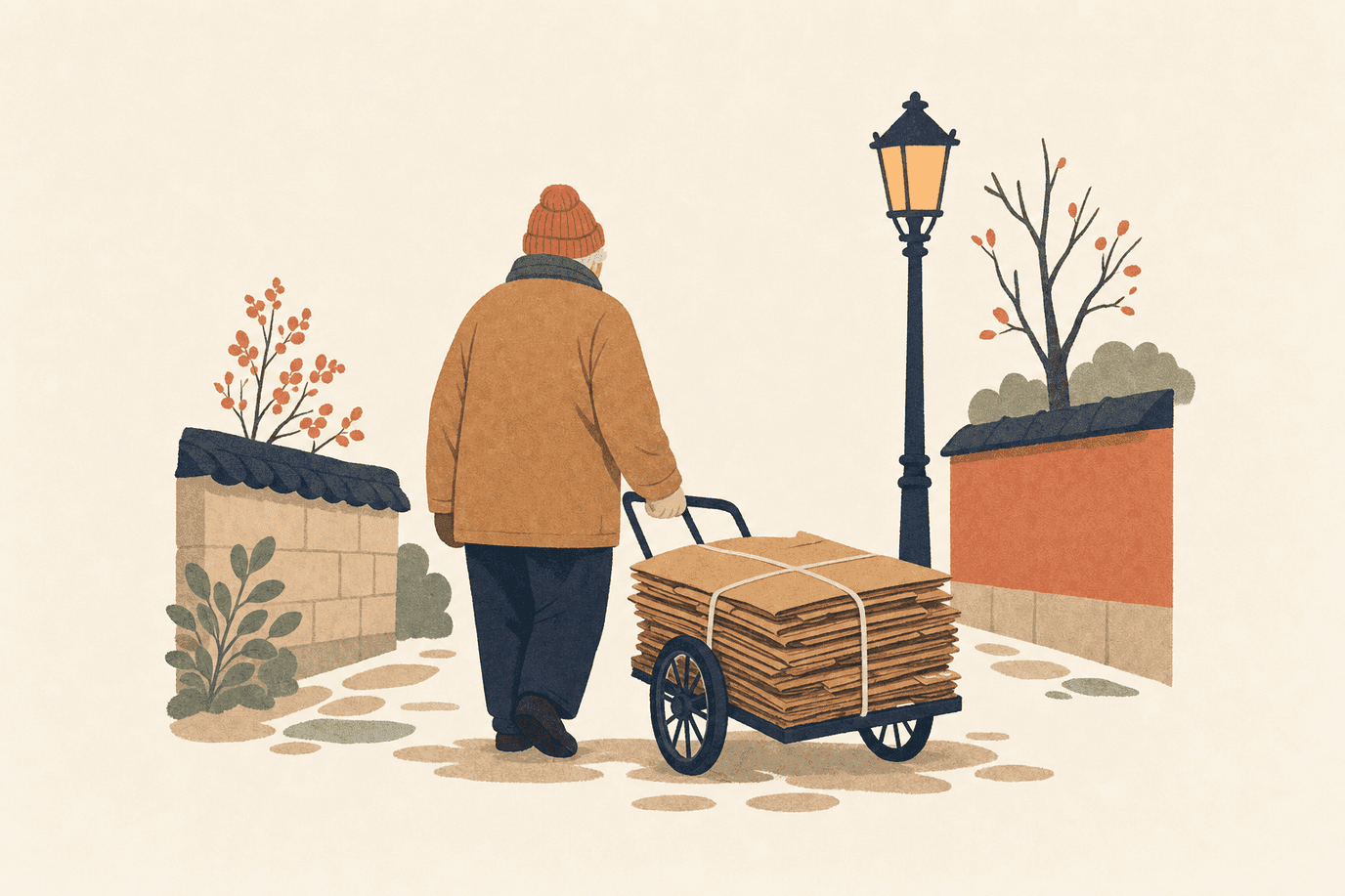

The cardboard collectors appear before most people are up. By 6 AM on any weekday in Seoul, you can see elderly men and women moving through apartment blocks and side streets with handcarts, lifting flattened cardboard boxes and bundling them with wire. Some are in their 70s. Many are in their 80s. A 2024 Ministry of Health and Welfare survey, the first of its kind, identified more than 14,800 Koreans aged 65 and older doing this work nationwide. Their average age was 78. Their average monthly income from all sources, including pensions and state benefits, was ₩766,000.

This is not a marginal story. It is the visible surface of the largest structural welfare gap in the OECD.

What you are seeing

The cardboard collectors are one sign. Others are harder to miss once you know what you are looking at.

The man at the overnight parking booth is almost certainly over 60. The woman cleaning the subway platform at 5 AM likely is too. The security guard in your apartment lobby who checks the visitor list in a plastic chair for 10 hours a day: check the age. Korea has the highest employment rate for people aged 65 to 69 in the OECD, at 57% in 2024, more than double the OECD average of 26% for the same group. The effective age at which Korean men fully exit the labor market is 67.4. For women, it is 69.6. Both are among the highest in the world.

This is not a sign of an energetic, purpose-driven elderly population. It is a sign of inadequate retirement income.

Korea's reserved subway seats for elderly and disabled passengers, the silver seats near each car door, fill up at 10 AM not just because older Koreans take leisure trips. Many are commuting to part-time shifts.

The number, in context

Nearly 4 in 10 Koreans aged 66 and older live below the relative poverty line. Statistics Korea's Social Trends Korea 2025 report puts the figure at 39.7%. OECD Pensions at a Glance 2025 puts it at approximately 40% using a slightly different methodology. The two figures measure the same condition.

The OECD average for the same age group is 14.8%.

Korea has held the worst position among OECD member countries continuously since 2009. The next worst countries, Estonia and Latvia, are both more than five percentage points behind.

The situation is worse for the oldest old. For Koreans aged 75 and above, the poverty rate exceeds 50%. This cohort predates even the 1995 rural expansion of the pension system and has had little or no pension income at all.

The rate has been improving, slowly. It peaked above 46% in 2013 and declined to around 37 to 38% by 2021. Then it ticked upward in 2022 and again in 2023, the first consecutive increase in a decade. The improvement has stalled.

The pension system is too young

The National Pension (국민연금) launched in January 1988, covering only companies with 10 or more employees. Coverage expanded in stages:

- 1992: workplaces with 5 or more employees

- 1995: rural workers, farmers, and fishermen

- 1999: urban self-employed and small workplaces

Universal coverage was not achieved until 1999. Anyone who was already in their late 40s or 50s in 1988 reached retirement age without completing the minimum 10-year contribution period required to receive any benefit at all. The current oldest cohort, those now aged 75 and above, retired before the system could reach them.

The numbers show the result. The average monthly National Pension benefit for an individual aged 65 and older is ₩695,000 (as of 2023, per Statistics Korea). The National Pension Research Institute estimates minimum monthly retirement costs for a couple at ₩2,166,000. An average couple both receiving National Pension income gets around ₩1,200,000 per month combined. That is 55% of what the Institute says a couple needs to live on.

The net pension replacement rate, meaning the pension a full-career average-wage worker receives as a share of their pre-retirement earnings, is 39% in Korea. The OECD average is 63%.

One figure sometimes cited as reassuring: Statistics Korea reported that 90.9% of Koreans aged 65 and older receive some form of pension. This requires context. That figure counts everyone receiving the National Pension, the Basic Pension (기초연금), any occupational pension, or any combination. Receiving a pension does not mean receiving enough to avoid poverty. The 40% poverty rate and the 90.9% coverage rate coexist because payout levels are too low.

The retirement gap

The Act on the Prohibition of Age Discrimination sets mandatory retirement (정년) at a minimum of 60. In practice, most large Korean companies require employees to leave at exactly age 60.

The National Pension does not begin paying out until age 63 for those born between 1964 and 1973. By 2033, that payout age rises to 65. The gap between being forced out of a career job and receiving any pension income is 3 to 5 years.

Unemployment insurance covers a maximum of 270 days for workers over 50. That is less than nine months of income.

What happens in the gap is documented in a July 2025 Human Rights Watch report titled "Punished for Getting Older." Workers re-enter the labor market at sharply lower wages. According to the report, citing Ministry of Employment and Labor data, workers aged 60 and older earned substantially less than younger workers, and a far higher share of older wage-earners hold non-regular, temporary, or part-time jobs than the workforce as a whole.

The jobs available are security, cleaning, janitorial work, construction day labor, food delivery, parking attendant, and building management. Some enter the government's Senior Employment Program (노인일자리사업), a subsidized job-placement scheme for people aged 65 and older. The 2026 plan targets more than 1.1 million positions. The Human Rights Watch report found that most program placements were unpaid public-service volunteer positions rather than paid employment, and only a small share were regular private-sector jobs. Monthly program wages for the volunteer tracks run well below the minimum wage.

There is also a gap before the mandatory retirement age itself. Statistics Korea's survey of older workers finds that most people leave their longest-held career job well before age 60. Informal pressures, restructuring, and voluntary departures under pressure push many out of their primary employer years before the legal retirement age. For those workers, the income gap before any pension begins is far longer than the 3 to 5-year gap that mandatory retirement alone would suggest.

The family-support model that broke

Korea historically did not rely on the state to support the elderly. It relied on children. The Confucian expectation that adult children would support aging parents was not just cultural. It was codified in law.

The Family Support Obligation rule (부양의무제) sat inside the Basic Livelihood Security Program (국민기초생활보장제도) for 60 years. A low-income elderly person whose adult child earned above a certain threshold was ineligible for welfare benefits, regardless of whether that child was actually providing support. The law assumed family support was happening and treated state assistance as redundant.

The rule was introduced in 1961. It was gradually phased out beginning in November 2017. It was permanently and fully repealed in October 2021. The repeal added approximately 400,000 newly eligible people to welfare programs almost immediately.

The underlying logic that the rule rested on collapsed across a single generation. South Korea urbanized faster than nearly any country on record. Adult children moved to Seoul. Elderly parents stayed in rural areas or smaller cities. The nuclear-household norm replaced the extended-household model within two decades. Korea's total fertility rate fell to 0.72 in 2023, the world's lowest. Smaller families mean fewer children to share any support burden. Adult children face their own costs: housing prices, education spending on their own children, unstable employment.

The old arrangement also quietly allowed the Korean state to under-invest in a pension system for decades. That political bargain has now expired. The families are gone, and the pension system is not yet ready.

Basic Pension: a floor, not a ladder

The Basic Pension (기초연금) is the state's main tool for reaching elderly Koreans the National Pension does not adequately serve. It is a means-tested monthly cash transfer for the bottom 70% of Koreans aged 65 and older.

The 2025 monthly amount is ₩342,510 per person. Plans announced by the Ministry of Health and Welfare call for raising this to ₩400,000 for low-income recipients in 2026.

Around 6.5 million elderly Koreans receive the Basic Pension as of 2023. It is now Korea's single largest welfare program, with spending that has climbed steeply over the past decade.

The 2026 eligibility thresholds: monthly recognized income below ₩2,470,000 for a single-person household, and below ₩3,952,000 for a couple household.

The problem with the Basic Pension is arithmetic. ₩342,510 a month is approximately what a week of groceries for one person costs in Seoul. It was designed as a supplement to sit on top of a National Pension. For the oldest cohort, who receive no National Pension at all, it is the entirety of their state income. The Human Rights Watch report calculated that the Basic Pension equals only about 16% of the 2024 national minimum wage.

Why elderly women have it worse

The elderly poverty rate for women aged 65 and older sits at around 43%. For men the same age, it is around 32%. The gap has widened over time, not narrowed.

Four structural factors drive this:

First, interrupted contribution histories. Women who took years out of formal employment to raise children accumulated few or no National Pension contribution years. A system that requires a minimum of 10 contribution years to pay anything at all hits women with career gaps hard.

Second, wage gap transmission. Women who did work in formal employment throughout their careers contributed at lower wages, producing lower pension payouts. The wage gap does not end at retirement. It compounds through it.

Third, widowhood. Korean women outlive Korean men. Many elderly women managed household finances through their husband's income. Once widowed, they inherit only a reduced survivor's benefit from the National Pension, not the full benefit their husband received.

Fourth, the household-head structure. Older social and legal frameworks treated men as the household head for purposes of pension, property, and welfare rights. Women who were economically dependent on that structure have no fallback outside it.

The 2025 National Pension reform added childbirth credits: 12 months of credited contribution for the birth of a first child. This helps women entering the workforce today build more complete pension records. It does nothing for the current elderly cohort.

What has been done

The policy response has three main components.

The Basic Pension has been Korea's primary lever. It rose from ₩200,000 in 2014 to ₩342,510 in 2025. Total spending more than tripled over the past decade. The planned increase to ₩400,000 for low-income recipients in 2026 is the next step.

The Family Support Obligation repeal in October 2021 removed a 60-year barrier to welfare eligibility. Around 400,000 people gained access to benefits they were previously denied. A residual means-testing threshold remains: adult children or parents who earn over ₩100 million annually or own property above ₩900 million can still render an elderly applicant ineligible. Critics argue the threshold is still too tight.

The 2025 National Pension reform, passed by the National Assembly on March 20, 2025, makes two meaningful structural changes. Contribution rates rise from 9% to 13% over eight years, beginning in 2026. The replacement rate rises to 43% for a worker with 40 contribution years. The fund's projected depletion date moves from 2056 to 2064. These are genuine improvements for workers who are young today. For people who are already retired, the reform changes nothing. The 43% replacement rate applies only to workers completing a full 40-year contribution record. No one currently aged 65 or older could have met that standard, because the system did not exist for the first part of their working lives.

Debate continues about raising the mandatory retirement age from 60 to 65, which would close the income gap between job loss and pension eligibility. As of June 2026, no such change has been enacted. Business groups oppose it on labor cost grounds. Younger workers' unions are cautious about potential effects on job openings.

What this means for you

The cardboard collector, the overnight parking attendant, the subway cleaner: these are not incidental details of urban life in Korea. They are the visible end of a policy timeline.

Korea industrialized faster than any country in history. Samsung and Hyundai are global names. K-pop generates billions in exports. The KOSPI is one of Asia's major indices. And nearly 4 in 10 elderly Koreans live below the poverty line. These two things coexist because the welfare state did not keep pace with the economic state. The pension system universalized in 1999. The extended family support structure collapsed in the same two decades. The generation that built the export economy retired into the gap between the two.

Japan is the useful comparison. Japan has a similar demographic profile: a fast-aging population, a low birth rate, high housing costs. Japan's elderly poverty rate is roughly half of Korea's. The difference is timing. Japan started building its pension system decades earlier and built a more complete safety net alongside it.

Korea entered what demographers call super-aged society status at the end of 2024, meaning 20% of the population is aged 65 and older. The National Pension system is still maturing. The youth population that funds the system is, on current birth rate trajectories, among the smallest of any wealthy country. The math of that combination is what drives the pension reform debate, the mandatory retirement age debate, and the Basic Pension spending debates that appear in Korean news regularly.

For a foreign resident in Korea, understanding this structure changes how you read several daily-life observations. The 70-year-old working the convenience store night shift. The 75-year-old woman walking 10 kilometers of streets with a cart. The reserved subway seats that are always occupied. These are not signs of a country that values the work ethic of its elderly. They are signs of a welfare system that arrived too late for the people who needed it most.

FAQ

What percentage of elderly Koreans live in poverty? Around 40% of Koreans aged 66 and older live below the relative poverty line, according to Statistics Korea's Social Trends Korea 2025 report and OECD Pensions at a Glance 2025. This is the highest rate among OECD member countries and nearly three times the OECD average of 14.8%.

Why do so many elderly Koreans work past retirement age? Most work out of financial necessity, not by choice. Korea's National Pension (국민연금) pays an average of ₩695,000 a month to individual recipients, which does not cover basic living costs in most cities. Many retirees also face a 3 to 5-year gap between mandatory retirement at 60 and the earliest pension payout age of 63. During that gap, part-time or informal work is often the only income source.

What is the Basic Pension and who gets it? The Basic Pension (기초연금) is a means-tested monthly cash benefit for the bottom 70% of Koreans aged 65 and older. The 2025 amount is ₩342,510 per month. Plans call for raising this to ₩400,000 for low-income recipients in 2026. As of 2023, around 6.5 million elderly Koreans receive it. It was designed as a supplement, not a living income on its own.

Why is the Korean pension system so underdeveloped? The National Pension (국민연금) only launched in 1988, and only for employees at larger companies. Agricultural workers and the self-employed were not covered until 1999. Anyone who was already in their 50s when the system launched reached retirement age without completing the 10-year minimum contribution period required to receive any benefit. The system is still maturing, and the current generation of elderly Koreans is bearing the cost of that timing.

Are elderly women worse off than elderly men in Korea? Yes, significantly. The elderly poverty rate for women is around 43%, compared to around 32% for men. Women had shorter formal careers and accumulated fewer pension contributions. Career women who did contribute earned lower wages, producing lower payouts. Many elderly women relied on their husband's income, and widowhood ends that household income while leaving them with only a reduced survivor's benefit from the National Pension.

What is the Family Support Obligation rule, and why was it controversial? The Family Support Obligation rule (부양의무제) was a clause in Korea's Basic Livelihood Security Program that could make a low-income elderly person ineligible for welfare if their adult children earned above a certain income threshold, even if those children were not actually sending any money. The rule dated from 1961. It was gradually phased out from 2017 and permanently repealed in October 2021. The repeal added approximately 400,000 newly eligible people to welfare programs.

Does owning property protect elderly Koreans from poverty? Owning an apartment does not protect against income poverty. Many elderly Koreans hold substantial housing assets built up over decades of property price appreciation, but assets do not pay monthly expenses. A government-backed reverse mortgage program (주택연금) lets homeowners aged 55 and older convert home equity into monthly payments, but uptake has remained very low, partly due to a strong cultural norm against spending down the family property.

Did the 2025 pension reform fix the elderly poverty problem? Not for the current elderly population. The 2025 National Pension reform raises contribution rates from 9% to 13% over eight years and lifts the replacement rate to 43% for a full-career worker. These changes help future retirees. They do almost nothing for people who are already 65 and older, because that cohort either contributed under the old rules or not at all. The reform extends the fund's solvency by about eight years, but it does not address the income gap that exists today.